When deciding if a 401(k) is right for you, there’s always one big question. Can my 401(k) lose money? The answer is deeper than you think.

Continue reading

When deciding if a 401(k) is right for you, there’s always one big question. Can my 401(k) lose money? The answer is deeper than you think.

Continue reading

The Setting Every Community Up for Retirement Enhancement (SECURE) 2.0 Act introduces groundbreaking reforms tailored to amplify the retirement planning capabilities of small businesses. By doing so, it charts a pathway for increased employee engagement and substantial financial growth. In this piece, we’ll delve into two pivotal enhancements that promise significant benefits for small businesses: the provisions for automatic enrollment and increased employee contributions.

1. Championing Automatic Enrollment: In a bid to stimulate proactive retirement planning, the SECURE 2.0 Act encourages businesses to adopt an automatic enrollment approach for their employees in retirement plans. Though employees retain the flexibility to opt-out, historical data underscores that auto-enrollment often propels participation rates upward.

2. Increased Contribution Cap: The Act goes a step further by raising the cap on the percentage of wages that employees can contribute to their retirement plans. By doing so, it not only amplifies the potential savings for employees but also allows businesses to offer more robust benefits when hiring.

Higher Employee Participation: By embracing automatic enrollment, small businesses can expect a surge in employee participation rates. Historically, retirement plans that feature auto-enrollment have seen substantially higher engagement, ensuring a more secure financial future for employees.

Higher Savings and Retention: Increased participation not only benefits employees. Small businesses can save as much as $100,000 a year in reduced employee turnover thanks to robust retirement plans. In industries where 401(k) benefits are less common, it can even improve retention by as much as 54%.

In conclusion, the SECURE 2.0 Act, with its emphasis on proactive enrollment and enhanced contribution capabilities, offers small businesses an unprecedented opportunity to save money and hire better. By leveraging these new provisions, businesses can not only ensure a brighter financial horizon for their employees but also enhance their retirement plan’s quality and reach.

Looking for more information?

We produced a complete guide on the subject and the implications at the state level. You will find valuable titled SECURE Act 2.0: Everything You Need to Know.

Hey there savvy savers!

It’s Emma, your go-to girl for all things finance and… cooking? That’s right! Today, we’re dishing out lessons from my kitchen that surprisingly reminded me of the principles of smart investing. My trusty air fryer, beyond serving up the absolute crispiest potatoes, turned out to be an unexpected teacher in the importance of consistency, both in the kitchen and in my investing journey with saveday.

My mom is an air-fryer-evangelist. She taught me all about how it could whip up healthier meals without excess oil. But when I started, much like diving into a new investment, I was both excited and skeptical. Yet as I experimented, a pattern emerged. The consistent heat circulation ensured that my dishes were cooked perfectly every time. No more soggy centers or burnt edges; just golden-brown perfection, bite after bite.

Moreover, consistently using the air fryer made me realize the savings I was racking up. Fewer dining-out expenses and reduced grocery bills (since I wasn’t wasting ingredients on my botched cooking experiments) were clear indicators of how consistency pays off.

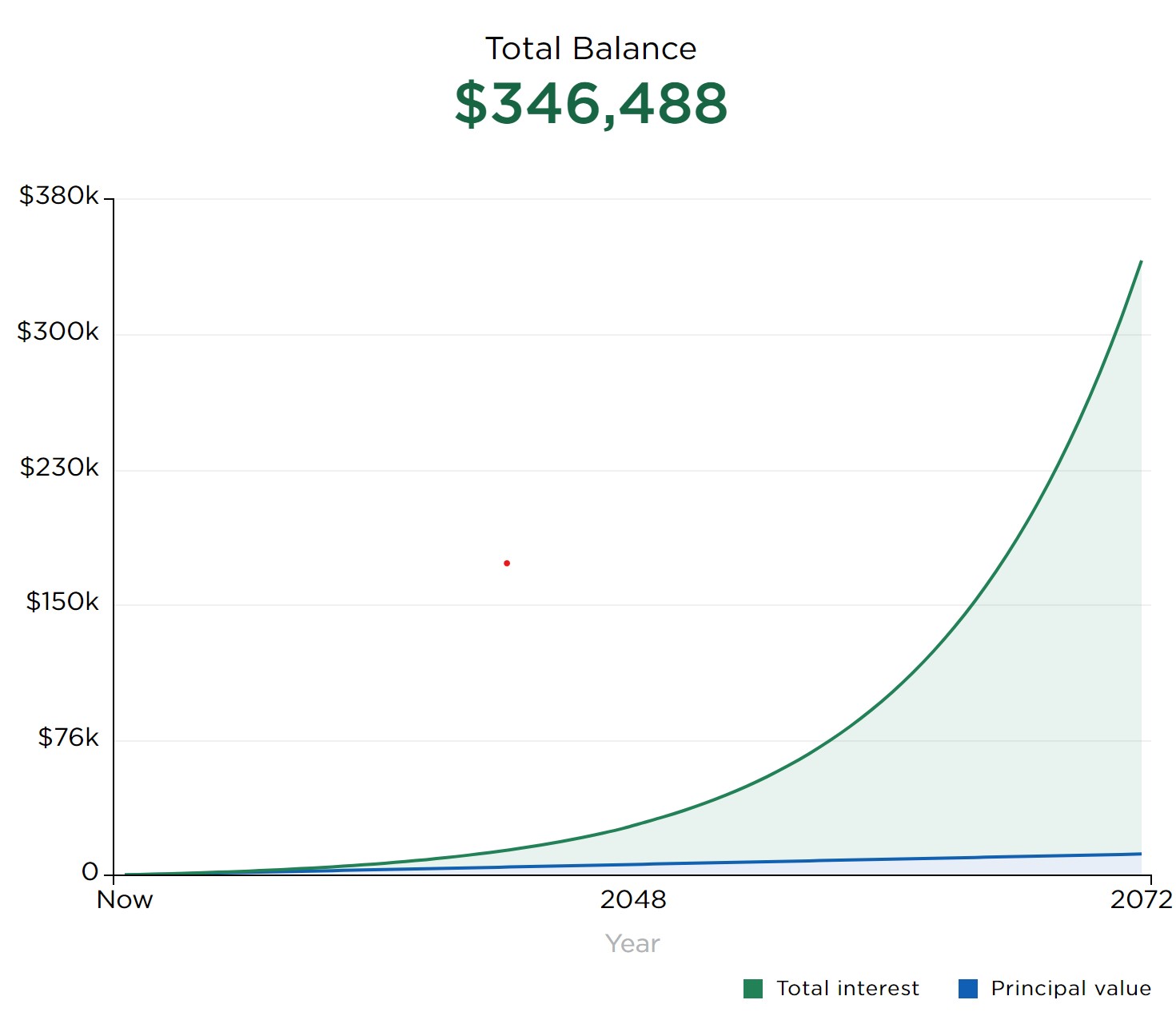

This got me thinking about my finance journey. Just as the steady circulation of the air fryer leads to optimal cooking, consistent investing with saveday helps optimize my financial growth. For me, it’s not about throwing all your money in at once or investing sporadically. It’s about the commitment to a regular, disciplined approach that yields results over time. Just take a look at how much a consistent $5 a week can grow over time.

Graph Generated by Nerdwallet

When you partner with saveday for your 401(k) plans, think of it as setting the temperature on your air fryer. You’re laying down the groundwork for a recipe that, with time and consistency, will provide delectable returns.

With my air fryer, small, consistent actions— like preheating, using minimal oil, or setting the timer— translated to mouth-watering meals every time. Similarly, in the realm of finance, regular contributions to your savings or 401(k) can lead to substantial growth over time, thanks to the magic of compound interest.

Just as you wouldn’t crank up the heat on your air fryer hoping to get quicker results (spoiler: like me, you’ll probably just burn your food), it’s essential not to seek shortcuts in investing. Instead, setting a consistent contribution rate and sticking to it, irrespective of market highs or lows, is a strategy that often proves successful in the long run.

In the end, my air fryer taught me that whether you’re cooking up crispy fries or a secure financial future, consistency is your best ally. By maintaining a disciplined approach, being patient, and understanding the process, you can ensure that your investments, much like your meals, turn out just right.

For more tips on mastering the art of saving, read on here!

Yours in flavor and finance,

-Emma

The SECURE 2.0 Act is legislation geared to help relieve the cost of 401(k) plans for small businesses. One of the clearest ways it does this is through tax incentives. When partnering with Saveday, these savings are compounded. But what exactly are these tax incentives, and how can they benefit small businesses?

Small businesses currently have the option to claim a tax credit for 50% of the startup costs involved in creating and administering a plan, with an annual maximum credit of $500. However, with the implementation of the SECURE 2.0 Act, this credit is increased. Now, businesses can claim a credit equal to either (a) $500 or (b) the lesser of $250 multiplied by the number of non-highly compensated employees eligible to participate in the plan, or $5,000. This change means that businesses can potentially access a maximum credit of $5,000 for a period of three years, which significantly offsets their initial costs.

In addition to the startup credits, the SECURE 2.0 Act introduces a new credit for small businesses that add automatic enrollment to their new or existing retirement plans. This credit is worth $500 and can be claimed for three years.

Businesses now have an extended period to adopt new retirement plans. So that means, rather than having to establish a plan by the end of the business year, businesses can set up a plan as late as their tax filing deadline, including extensions. This flexibility can assist in better financial planning for the tax credits.

Overall, the introduction of enhanced tax incentives for small businesses in SECURE 2.0 is a clear nod towards promoting retirement savings and making it more affordable for businesses to provide such plans. By partnering with a platform like saveday, which already minimizes costs, small businesses can leverage these incentives to the fullest, offering robust retirement benefits without a heavy financial burden.

Ready to learn more about how a 401(k) can transform your small business? Read more here.