This detailed guide is designed for small business owners and SMB leaders. It offers a clear roadmap to navigate the complexities of setting up a 401(k).

Continue reading

This detailed guide is designed for small business owners and SMB leaders. It offers a clear roadmap to navigate the complexities of setting up a 401(k).

Continue reading

When deciding if a 401(k) is right for you, there’s always one big question. Can my 401(k) lose money? The answer is deeper than you think.

Continue reading

The Setting Every Community Up for Retirement Enhancement (SECURE) 2.0 Act introduces groundbreaking reforms tailored to amplify the retirement planning capabilities of small businesses. By doing so, it charts a pathway for increased employee engagement and substantial financial growth. In this piece, we’ll delve into two pivotal enhancements that promise significant benefits for small businesses: the provisions for automatic enrollment and increased employee contributions.

1. Championing Automatic Enrollment: In a bid to stimulate proactive retirement planning, the SECURE 2.0 Act encourages businesses to adopt an automatic enrollment approach for their employees in retirement plans. Though employees retain the flexibility to opt-out, historical data underscores that auto-enrollment often propels participation rates upward.

2. Increased Contribution Cap: The Act goes a step further by raising the cap on the percentage of wages that employees can contribute to their retirement plans. By doing so, it not only amplifies the potential savings for employees but also allows businesses to offer more robust benefits when hiring.

Higher Employee Participation: By embracing automatic enrollment, small businesses can expect a surge in employee participation rates. Historically, retirement plans that feature auto-enrollment have seen substantially higher engagement, ensuring a more secure financial future for employees.

Higher Savings and Retention: Increased participation not only benefits employees. Small businesses can save as much as $100,000 a year in reduced employee turnover thanks to robust retirement plans. In industries where 401(k) benefits are less common, it can even improve retention by as much as 54%.

In conclusion, the SECURE 2.0 Act, with its emphasis on proactive enrollment and enhanced contribution capabilities, offers small businesses an unprecedented opportunity to save money and hire better. By leveraging these new provisions, businesses can not only ensure a brighter financial horizon for their employees but also enhance their retirement plan’s quality and reach.

Looking for more information?

We produced a complete guide on the subject and the implications at the state level. You will find valuable titled SECURE Act 2.0: Everything You Need to Know.

Hey there savvy savers!

It’s Emma, your go-to girl for all things finance and… cooking? That’s right! Today, we’re dishing out lessons from my kitchen that surprisingly reminded me of the principles of smart investing. My trusty air fryer, beyond serving up the absolute crispiest potatoes, turned out to be an unexpected teacher in the importance of consistency, both in the kitchen and in my investing journey with saveday.

My mom is an air-fryer-evangelist. She taught me all about how it could whip up healthier meals without excess oil. But when I started, much like diving into a new investment, I was both excited and skeptical. Yet as I experimented, a pattern emerged. The consistent heat circulation ensured that my dishes were cooked perfectly every time. No more soggy centers or burnt edges; just golden-brown perfection, bite after bite.

Moreover, consistently using the air fryer made me realize the savings I was racking up. Fewer dining-out expenses and reduced grocery bills (since I wasn’t wasting ingredients on my botched cooking experiments) were clear indicators of how consistency pays off.

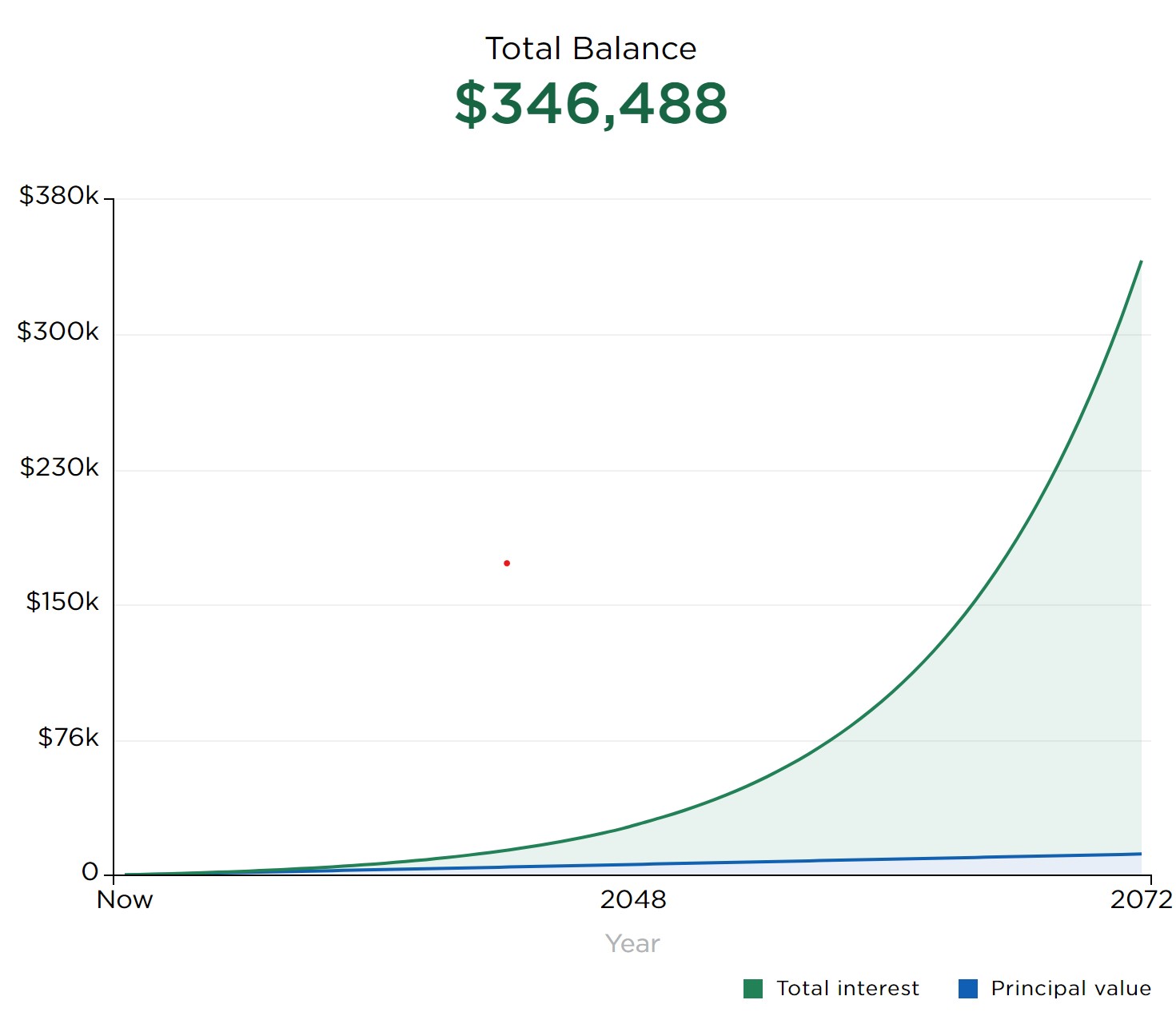

This got me thinking about my finance journey. Just as the steady circulation of the air fryer leads to optimal cooking, consistent investing with saveday helps optimize my financial growth. For me, it’s not about throwing all your money in at once or investing sporadically. It’s about the commitment to a regular, disciplined approach that yields results over time. Just take a look at how much a consistent $5 a week can grow over time.

Graph Generated by Nerdwallet

When you partner with saveday for your 401(k) plans, think of it as setting the temperature on your air fryer. You’re laying down the groundwork for a recipe that, with time and consistency, will provide delectable returns.

With my air fryer, small, consistent actions— like preheating, using minimal oil, or setting the timer— translated to mouth-watering meals every time. Similarly, in the realm of finance, regular contributions to your savings or 401(k) can lead to substantial growth over time, thanks to the magic of compound interest.

Just as you wouldn’t crank up the heat on your air fryer hoping to get quicker results (spoiler: like me, you’ll probably just burn your food), it’s essential not to seek shortcuts in investing. Instead, setting a consistent contribution rate and sticking to it, irrespective of market highs or lows, is a strategy that often proves successful in the long run.

In the end, my air fryer taught me that whether you’re cooking up crispy fries or a secure financial future, consistency is your best ally. By maintaining a disciplined approach, being patient, and understanding the process, you can ensure that your investments, much like your meals, turn out just right.

For more tips on mastering the art of saving, read on here!

Yours in flavor and finance,

-Emma

The SECURE 2.0 Act is legislation geared to help relieve the cost of 401(k) plans for small businesses. One of the clearest ways it does this is through tax incentives. When partnering with Saveday, these savings are compounded. But what exactly are these tax incentives, and how can they benefit small businesses?

Small businesses currently have the option to claim a tax credit for 50% of the startup costs involved in creating and administering a plan, with an annual maximum credit of $500. However, with the implementation of the SECURE 2.0 Act, this credit is increased. Now, businesses can claim a credit equal to either (a) $500 or (b) the lesser of $250 multiplied by the number of non-highly compensated employees eligible to participate in the plan, or $5,000. This change means that businesses can potentially access a maximum credit of $5,000 for a period of three years, which significantly offsets their initial costs.

In addition to the startup credits, the SECURE 2.0 Act introduces a new credit for small businesses that add automatic enrollment to their new or existing retirement plans. This credit is worth $500 and can be claimed for three years.

Businesses now have an extended period to adopt new retirement plans. So that means, rather than having to establish a plan by the end of the business year, businesses can set up a plan as late as their tax filing deadline, including extensions. This flexibility can assist in better financial planning for the tax credits.

Overall, the introduction of enhanced tax incentives for small businesses in SECURE 2.0 is a clear nod towards promoting retirement savings and making it more affordable for businesses to provide such plans. By partnering with a platform like saveday, which already minimizes costs, small businesses can leverage these incentives to the fullest, offering robust retirement benefits without a heavy financial burden.

Ready to learn more about how a 401(k) can transform your small business? Read more here.

Welcome back, savvy savers!

It’s Emma here, serving up fresh insights straight to your screen. I (like many of us) occasionally pull myself into the digital whirlwind of Tik Tok- the platform where dancing and financial advice can coexist peacefully! That’s how I stumbled upon the viral 100 Envelopes Challenge. As an ardent believer in the power of my saveday 401(k), I had to put the numbers to the test. Which is better at saving me money: the 100 Envelopes Challenge or my trusty 401(k)?

Here’s the brief rundown: whoever wants to participate will number envelopes from 1 to 100. Every payday, an envelope is picked at random, and the participant must stash the amount of cash corresponding to its number inside. Sounds straightforward, right? Now, let’s break down its savings potential.

If you follow this challenge faithfully after each payday on a bimonthly basis, you’d amass $5,050 over 50 months. Not bad for a social media challenge!

Now, let’s see if it holds up to the mighty saveday 401(k)…

Investing in a 401(k) does more than just save. It helps your money grow. That growth is powered by compounding. Let’s see what a 10% return on your account that’s compounded monthly can look like with $5,050.

After 50 months more that cash will be worth $7,642.04 without you having to lift another finger. That’s $2,592.04 more than if you had just let it sit for all that time.

But what if you decided to do the 100 Envelope Challenge and 401(k) investing all at once? Let’s see what you can do when you add $5,050 for another 50 months.

After waiting, $19,206.55 would all be yours.

If you decide to wait and let it grow for an even longer time, let’s say 30 years, you will have earned $251,777.07 by the end of it.

That’s $239,085.03 in pure profit.

To sum it all up, I think the 100 Envelope Challenge can be an amazing introduction to your savings potential. But to really unlock your supercharged financial future, a 401(k) is the way to go. Coupling your saveday superpower with this viral challenge can lead to big savings later on. Overall, I’m calling it a win for 401(k)s and a win for people like us trying to save.

Hungry for more saving insight? Saveday has a buffet of tips and tricks ready for your tastebuds over at their blog. Read on to discover how delicious your future can be!

Happy Saving,

-Emma

For small businesses, offering competitive retirement benefits can be costly and complex. But the tides are changing with the SECURE Act 2.0. This recent legislation introduces enhanced Multiple Employer Plans (MEPs). This allows businesses, irrespective of their size or industry, to pool resources and provide joint 401(k) plans to their employees.

At its core, MEPs under the SECURE Act 2.0 offer a streamlined approach to retirement planning, thus making it more accessible and efficient for small businesses. Here’s why that matters:

Joining a MEP lessens the administrative burden placed on small businesses. In essence, most responsibilities are shouldered by the MEP provider. This consequently minimizes paperwork and compliance issues for participating employers.

Pooling resources with MEPs often means reduced fees and potentially superior investment choices, which leads to noteworthy savings for small businesses.

MEPs empower small businesses to present retirement plans that rival those of big corporations. Therefore, this helps ensure they attract and retain talented employees.

The collaborative nature of MEPs diminishes fiduciary risks for individual employers, as these are often shared or completely handled by the MEP provider.

Your partnership with saveday can make navigating these changes even simpler. We’re designed to guide businesses through retirement nuances. With the SECURE Act 2.0, and the potential of MEPs, small businesses are in a stronger position than ever to secure a better retirement future for their workforce. You can help ensure a brighter future for your team by partnering with saveday today.

Hey savvy savers!

Emma here, back with another dose of financial wisdom. Today, I’m diving deep into a term that floats around a lot with 401(k)s: vesting. Unfortunately, it’s not about thrifting a quirky vest with your friends (but I’m free Saturday if that sounds fun to anyone else). Vesting, in the 401(k) world, plays the role of determining when you officially “own” your retirement fund.

Vesting refers to the amount of time you need to be with your employer before you “own” or have the full right to the employer contributions made to your 401(k) account. Now, you always have 100% ownership of the funds you contribute from your paycheck. The schedule comes into play with the additional funds your employer might toss into the mix.

Vesting is an incentive. Companies want talented employees (like us) to stick around. Offering a 401(k) match is attractive, but they might not want to hand over all those funds immediately if there’s a change you might leave early. The vesting schedule ensures that you’re rewarded the longer you stay.

First things first: check your 401(k) plan details or chat with HR. Know where you stand. If you’re considering a job change and you’re close to being fully vested, it might be worth waiting a bit, so you don’t leave money behind.

Saveday has been a lifesaver for working through nitty gritty details like these. Find out more tips and tricks with their blog here.

Until next time!

-Emma

Welcome back, savvy savers!

Emma here, with a fresh coffee and fresh insights! Let’s get real, millennials. It seems like every headline is telling us about the future we can’t have. Ready to flip the script? This blog post is about becoming the saver you want to be, even with student loans. It really is possible to save without compromising the little things you love. Let me show you how saveday did that for me.

Millennials, often tagged as the “student loan generation”, find themselves in a tight bind. On one hand, there is the burgeoning weight of student loans, on the other, there’s the pressing need to kick start retirement planning. It may seem like standing at the crossroads, but guess what? You can still have it all.

Let’s be real. This “adulting” thing is hard. Saveday has helped me know that I’m not alone when it comes to finance. Their intuitive tools and resources are designed to empower people like us. It really does make saving smoother and more attainable. Here’s two ways you can seize the savings today…

At the end of the day, remember your financial success journey is a marathon, not a sprint. With the right planning and support, you can dance gracefully through student loans and debts to earn the blossoming retirement garden you deserve.

Here’s to mastering the art of financial balance, one step at a time!

Let’s get saving!

-Emma